On this page

This is Part 2 of 3 in Understanding Today's Crypto Market. If you haven't read Part 1, start with What actually happened to crypto?.

How crypto rebuilt itself

After the reset, something unusual happened. While much of the public conversation around crypto focused on collapse, lawsuits, bankruptcies and volatility, large parts of the industry continued evolving underneath the surface. From the outside, crypto often appeared stuck in crisis after 2022 — confidence damaged, trust deteriorated, the speculative boom apparently imploded under its own excess. But developers continued building, infrastructure continued improving, and the market that slowly rebuilt no longer looked quite the same as the one that had entered the previous cycle.

The rebuild did not happen all at once. It happened gradually, across different parts of the ecosystem, often while attention remained focused elsewhere. Decentralised finance was one of the first areas to change. Earlier phases of DeFi had often been driven by unsustainable yields, aggressive incentives and poorly understood risk, and when those systems failed in 2022, confidence in that model deteriorated rapidly. The next phase looked different. Developers focused on transparency, on visible collateral structures, and on systems where reserves could be publicly audited on-chain in real time. Resilience mattered more than speed of expansion, and users became more aware of leverage, liquidity risk and counterparty exposure than they had been during the previous cycle.

Blockchain infrastructure itself improved alongside it. Ethereum scaling networks, commonly known as Layer 2s, expanded rapidly as developers worked to reduce transaction costs and improve network efficiency. What had once felt experimental began to function more like everyday financial plumbing — cheaper to use, faster to settle, and capable of supporting activity that earlier infrastructure simply could not.

Stablecoins quietly became infrastructure

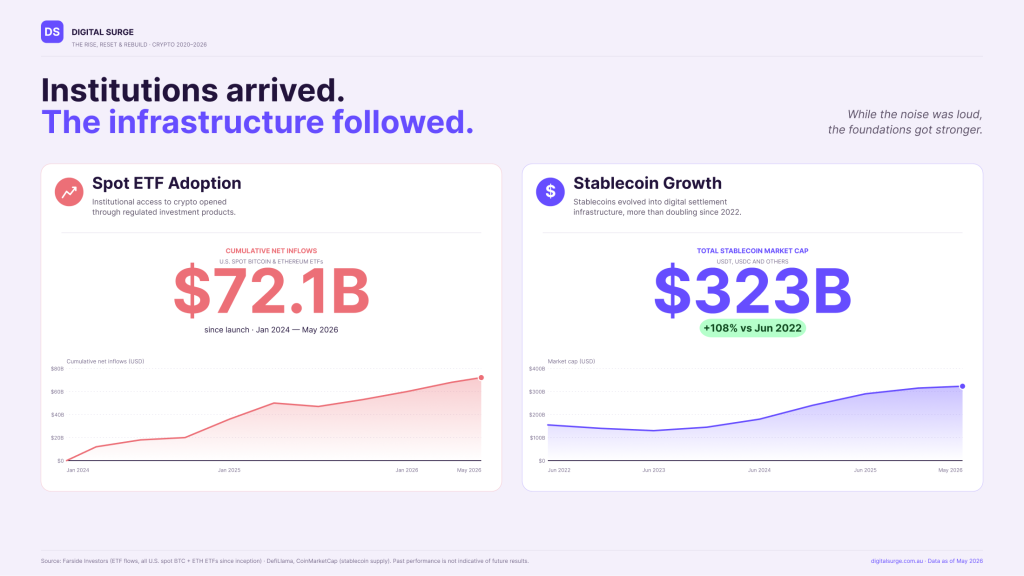

One of the clearest examples of this rebuilding process was the rise of stablecoins. Originally designed as trading tools within crypto markets, they evolved into something much larger: digital settlement infrastructure operating across the internet. Businesses, traders and individuals began using stablecoins for reasons that had little to do with speculation — faster settlement, 24/7 transferability, and easier access to US dollar-denominated assets across regions where traditional banking systems were slower or less accessible. Over time, they started functioning less like crypto products and more like internet-native dollars.

Major payment and financial companies began paying closer attention. Stripe expanded its stablecoin-related initiatives, PayPal launched its own US dollar stablecoin, and traditional payment networks explored blockchain-based settlement systems and tokenised financial infrastructure. While much of the public conversation remained focused on speculation, stablecoins quietly became one of the most practical and widely used areas of crypto itself.

The broader macro environment also played a role. Inflation concerns, geopolitical instability and rising government debt levels pushed investors globally toward discussions around scarce assets, alternative financial infrastructure and long-term monetary resilience. Gold experienced one of its strongest periods in decades, and Bitcoin entered the same macroeconomic conversation. For many institutions, the discussion around Bitcoin was no longer purely technological — it revolved around scarcity, liquidity, monetary policy and global capital flows.

Speculation transformed

Speculation, however, did not disappear.

If anything, it evolved into something faster, more social and even more internet-native than before.

Memecoins remained one of the highest-engagement sectors of the market, but the centre of activity shifted significantly. PEPE reignited meme speculation in 2023, followed by BONK, POPCAT and Dogwifhat (WIF) emerging from the rapidly growing Solana ecosystem.

Solana’s low transaction costs and fast settlement speeds made it the natural environment for highly speculative token launches, sometimes with hundreds of new assets appearing within a single day.

By 2024, platforms like Pump.fun dramatically lowered the barrier to creating tokens. Memes, livestreams and online communities could suddenly generate trading activity around entirely new assets within hours.

AI-themed memecoins such as GOAT and FARTCOIN became one wave of speculation, while community-driven assets like SPX6900 gained traction through internet culture and viral momentum. Celebrity-linked and politically branded tokens followed, culminating in the launch of the TRUMP memecoin in early 2025, one of the most-discussed moments of the cycle.

None of this meant speculation had become safer or more sustainable. But it revealed something important about crypto itself: even as institutions entered the market more formally, crypto remained deeply connected to internet culture, online communities, humour, identity and attention.

That culture survived the reset too.

Not every internet-native project disappeared either.

While many NFT collections faded alongside the speculative boom, a smaller number adapted rather than collapsing completely. Instead of focusing purely on digital asset trading, some projects expanded into merchandise, licensing, retail partnerships and broader consumer brands.

Pudgy Penguins became one of the clearest examples of this transition, evolving from a speculative NFT collection into a wider internet-native consumer brand with mainstream retail visibility.

Most projects from the NFT era did not survive. The ones that did increasingly looked less like speculative assets and more like startup brands attempting to build long-term businesses around community and intellectual property.

Altcoins entered a different era

Another major shift involved the structure of the altcoin market itself. In earlier crypto cycles, broad "alt seasons" often saw large parts of the market rise together as capital rotated rapidly from Bitcoin into smaller assets, and many participants entered the 2023-2025 cycle expecting a similar pattern to emerge again.

But the market had changed.

The number of tradable crypto assets had expanded dramatically, with new tokens launching constantly across meme platforms, decentralised exchanges and emerging ecosystems. Attention fragmented across thousands of competing narratives, communities and speculative assets, and market activity often concentrated into shorter, faster and more isolated bursts rather than the broad-based rallies that had defined previous cycles.

The structure of altcoins themselves also received greater scrutiny. Investors became more aware of token inflation, venture capital allocations, emissions schedules and team unlocks that could gradually increase supply over time, and fully diluted valuations became part of mainstream crypto discussion as users looked more closely at how token economics affected long-term sustainability.

This shift produced unusual outcomes. In some cases, projects reached new price highs while simultaneously carrying significantly larger circulating supplies and much higher overall market capitalisations than they had during previous cycles. XRP became one example often discussed across the market — it reclaimed and slightly exceeded its 2018 all-time high, but its circulating supply and overall valuation had grown dramatically in the years since, making like-for-like comparisons across cycles much harder.

Many projects continued building through the reset period. But the reality also became clear: not every token would survive long term. As the market matured, understanding what an altcoin actually did, how its supply functioned and whether adoption was genuinely growing became far more important than simply assuming every asset would eventually rise alongside Bitcoin.

The institutional and regulatory turn

As crypto rebuilt itself, the shift extended well beyond market behaviour and became political, institutional and geopolitical too. After the collapses of 2022, governments and regulators globally began paying far closer attention to how crypto businesses operated, how customer assets were handled and how digital assets would fit within existing financial systems.

In the United States, SEC Chair Gary Gensler became one of the defining regulatory figures of the period as the SEC pursued an aggressive, enforcement-led approach toward large parts of the crypto industry. Lawsuits, investigations and regulatory uncertainty created ongoing tension between regulators and crypto companies throughout much of 2023 and 2024. But the conversation gradually began shifting. Rather than debating whether crypto would survive at all, policymakers focused on how digital assets would ultimately integrate into the financial system.

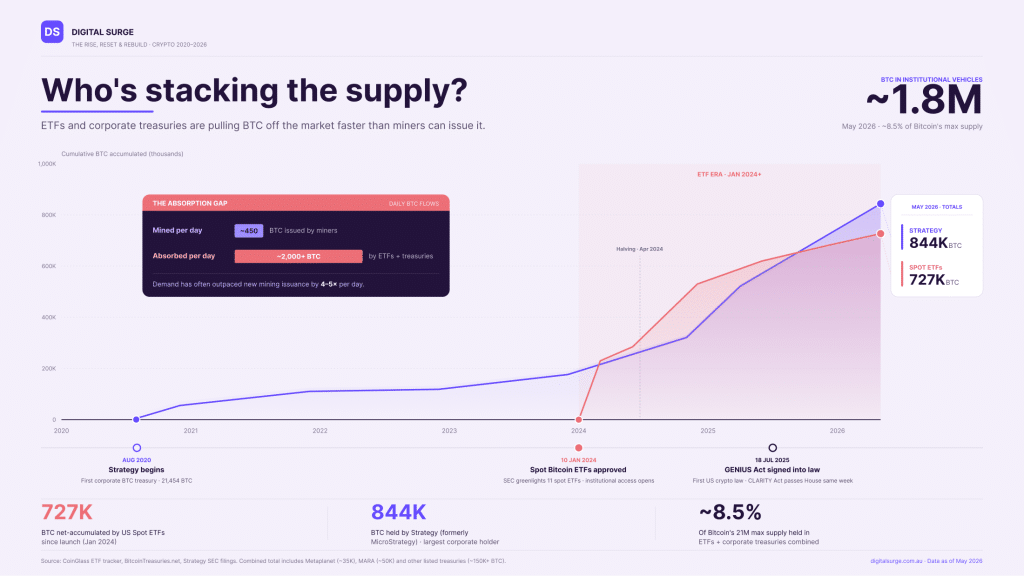

The approval of spot Bitcoin ETFs in January 2024 marked one of the clearest turning points. BlackRock, Fidelity and several of the world's largest asset managers entered the market directly, fundamentally changing how Bitcoin could be accessed through traditional financial infrastructure. For the first time, Bitcoin exposure became available through regulated investment products integrated into brokerage accounts, retirement systems and traditional wealth management platforms already used throughout conventional finance.

Later that year, Bitcoin crossed US$100,000 for the first time, a major psychological milestone in its transition from speculative technology into mainstream macroeconomic discussion. Only a year earlier, many crypto businesses had struggled to maintain banking access following the collapse of Silvergate and Signature Bank. By 2024 and 2025, some of the world's largest financial institutions were actively building products around Bitcoin exposure instead. Morgan Stanley became one of the first major Wall Street banks to allow financial advisers to offer spot Bitcoin ETF access to eligible clients, reflecting how rapidly institutional participation was evolving.

The political environment surrounding crypto also became more important globally. In the United States, proposals such as the CLARITY Act and broader stablecoin legislation reflected growing efforts to establish clearer rules around digital assets, market structure and blockchain-based financial systems, while the GENIUS Act further accelerated discussions around stablecoin regulation and the future role of digital payment infrastructure within the US financial system. Bitcoin itself entered sovereign and geopolitical discussions as governments debated digital asset reserves, strategic positioning and financial competitiveness in an increasingly digital global economy.

Australia experienced its own version of this transition. Following the turbulence of the reset period, Australian regulators and policymakers focused on licensing, custody standards, consumer protection and operational resilience across the local industry. The Corporations Amendment (Digital Assets Framework) Bill 2025, passed in April 2026, became one of the clearest signs that Australia was moving toward a more formalised regulatory structure for digital assets and exchanges. The result was a very different environment from the largely unstructured expansion phase that had defined earlier crypto cycles.

Corporate treasuries and tokenisation

As institutional participation expanded, some companies began treating Bitcoin less as a speculative trade and more as a long-term treasury asset. Strategy (formerly MicroStrategy) remained the most prominent example, continuing to accumulate Bitcoin at unprecedented scale and eventually holding more than 4% of Bitcoin's total supply by mid-2026. Over time, other public companies and investment firms also began exploring digital asset treasury strategies as part of broader capital allocation models.

Japan's Metaplanet became one of the most-discussed examples outside the United States as it accelerated Bitcoin accumulation through its corporate treasury strategy. GameStop also entered the conversation after announcing Bitcoin purchases for its balance sheet, highlighting how crypto treasury exposure was spreading into a wider range of public companies and internet-native brands.

The trend extended beyond Bitcoin itself. A growing number of firms explored Ethereum-focused treasury strategies, with companies such as BitMine publicly accumulating ETH and discussing blockchain-based financial infrastructure. Other firms experimented with treasury exposure tied to altcoins and emerging digital asset ecosystems. What began as an outlier strategy earlier in the decade had become a category of its own.

The shift extended beyond company balance sheets too. Tokenisation and real-world assets (RWAs) became some of the fastest-growing areas of institutional blockchain development, with financial institutions exploring how traditional assets such as treasury products, bonds, funds and credit markets could operate on blockchain infrastructure. BlackRock's BUIDL fund became one of the clearest examples of this transition, reflecting how tokenisation evolved from a theoretical concept into active financial experimentation involving some of the world's largest institutions.

Maturity did not eliminate risk

The rebuild made crypto more institutional, more regulated and more infrastructure-focused, but it did not eliminate many of the market's underlying risks. Large-scale hacks and exploits continued to remind the industry that operational security remained one of the sector's biggest challenges, with the Bybit exploit in 2025 becoming one of the largest hacks in crypto history and reinforcing how serious vulnerabilities could still emerge within major platforms and infrastructure providers. DeFi exploits and smart contract vulnerabilities also continued across parts of the ecosystem, particularly within newer or experimental protocols where innovation often moved faster than security testing and risk management.

Periods of extreme volatility remained part of the market too. In October 2025, one of the largest crypto liquidation events on record cascaded through the market within hours, highlighting how leverage, automation and trading infrastructure could still amplify instability during periods of stress.

Longer-term risks also began to attract more attention, with quantum computing emerging as one of the most discussed. The cryptographic signatures securing Bitcoin, Ethereum and most digital assets were designed in a pre-quantum era, and as quantum hardware advanced, the prospect of a future "Q-Day" — when a sufficiently powerful machine could break existing standards — pushed the industry to begin exploring post-quantum cryptography and quantum-resistant alternatives. The threat remained years away, but the implications for a sector built on unbreakable keys were significant enough that the conversation had moved firmly into the mainstream.

The market that rebuilt after the reset may have become more mature, more institutional and more infrastructure-focused. But it did not become risk-free.

Two parallel realities

The market that emerged after the reset no longer fits neatly into the old narratives that defined earlier cycles. One side remains speculative, internet-native and heavily driven by memes, online communities and rapid narrative shifts. The other is becoming more institutional, infrastructure-focused and connected to traditional finance, payments and digital settlement systems. Both realities now exist simultaneously within crypto.

Speculation still exists. Volatility still exists. Internet culture still shapes large parts of the market. But underneath all of that, crypto increasingly resembles an emerging layer of financial and technological infrastructure developing in parallel with the traditional system.

That coexistence may ultimately define this era of crypto more than any single price cycle.

This is Part 2 of 3 in Understanding Today’s Crypto Market. Continue reading: Part 3, Engaging With Crypto Differently Today. How many users are engaging with crypto, and why participation increasingly looks more measured than it did during previous cycles.